In our 4th quarter Investment Update last year, like many, we acknowledged the challenges heading into 2023, particularly concerning additional rate hikes and the risk that the Federal Reserve could unduly weaken the economy in its campaign to defeat inflation. As our investment strategies focus more on the prospects of individual companies, we also highlighted the perils of overconfidence in making year-end prognostications, especially considering the positive consensus outlook that greeted 2022 and predictions of a recession in 2023. After a terrific rebound year for stocks, investors are once again optimistic about stock returns in 2024. We will discuss below some of the valid reasons behind this optimism, while also observing where caution may be appropriate.

2023

It is helpful to try to understand why the 2023 results exceeded almost everyone’s expectation. While the stock market does not always mirror the economy, explaining the resilience of the economy is a good place to start. Two important facets of the economy surprised:

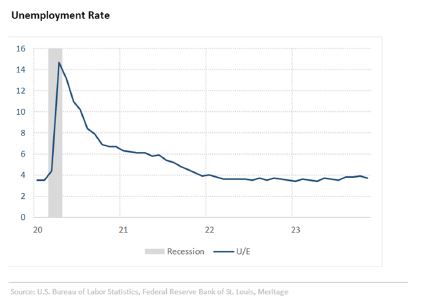

First, the rate of inflation declined faster than expected. The prices of services joined the decline in goods, while supply chain disruptions largely resolved. Less pressure on the consumer’s wallet helped, while unemployment rates stayed low and wage growth remained healthy. China’s economic weakness also alleviated pressure on the prices of goods.

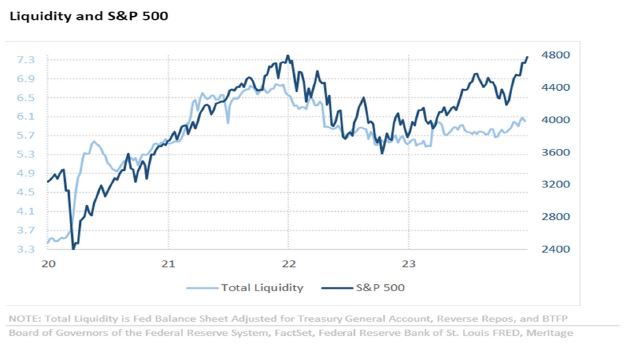

Second, the fastest rate hikes in 40 years had a lesser effect on consumers and businesses than expected. Part of this was due to existing home mortgages and corporate debt that was financed when rates were much lower. Economists also underestimated the amount of liquidity that remained from pandemic-related stimulus. Additionally, the Fed’s plan to shrink the money supply was disrupted when they came to the aid of the banking system during the mini-crisis in March. All these left financial conditions far less restrictive than what had been seen in previous tightening cycles. Looking forward, ongoing government spending commitments will continue to provide a liquidity buffer against higher interest rates.

Year-end rally correlated with the increase in financial liquidity

The economy aside, the fundamental performance of corporations in general was not distinguished in terms of earnings growth, but earnings and revenues did come in better than expected by industry analysts. Additionally, the excitement around the prospects of artificial intelligence and the accompanying demand for hardware, software, and semiconductors was a significant catalyst for the tech industry’s market-leading performance and improved investor sentiment.

The economy aside, the fundamental performance of corporations in general was not distinguished in terms of earnings growth, but earnings and revenues did come in better than expected by industry analysts. Additionally, the excitement around the prospects of artificial intelligence and the accompanying demand for hardware, software, and semiconductors was a significant catalyst for the tech industry’s market-leading performance and improved investor sentiment.

2024

As we think about the year ahead, unlike where markets stood a year ago, current stock prices reflect much of what can go right in the coming year. Our outlook is constructive, but our expectations are more moderate, given the possibility that not everything falls into place as now seems expected.

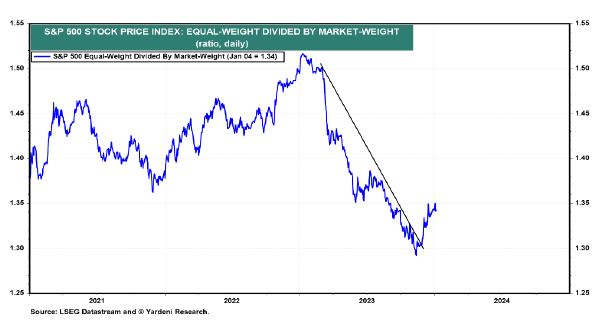

We take encouragement from the 4th quarter rally in stocks that broadened beyond the major mega-cap companies (Apple, Microsoft, Alphabet, Nvidia, Amazon, Meta and Tesla). A more inclusive market is typically a good sign for continued market strength.

The bounce in the equal-weighted S&P 500 was triggered by the Fed’s dovish remarks in November

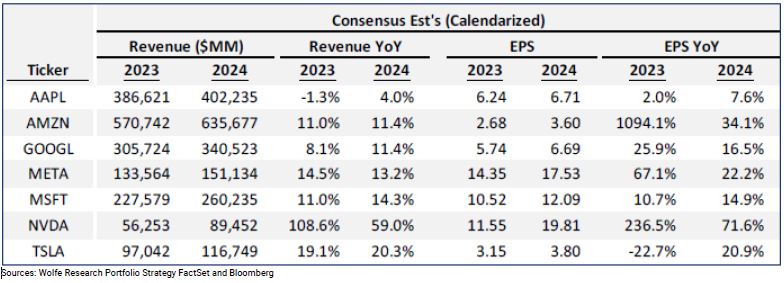

There was a lot of discussion about mega-cap stocks this year (the largest now known as the Magnificent Seven). They had superior earnings growth compared to the broad market and their strong balance sheets and enviable business models gave investors comfort this past spring when it looked like bank failures could again derail the markets. We questioned whether there was a diversification risk in having 30% of a “market” index concentrated in just seven companies. And we ask today, under what circumstances would these companies again dominate stock returns.

In a positive market environment, we think that would be asking a lot, given the group’s average return last year of 73%. Still, we expect investors will be attracted to their prospects of above-average earnings growth. In a negative environment there is valuation risk, as we saw in 2022. There is also a scenario where their defensive characteristics hold up, notwithstanding their premium valuation. That said, we believe the best opportunities to add value in 2024 will be outside of the market’s largest holdings.

“Magnificent 7” Expectations Are Running Very High!

As usual, there are a myriad of risks that could reclaim the narrative at any time. Most of these concerns are well understood and not particularly new. Key among them include the lag effect of rate hikes simply postponing the recession, inflation being too sticky to reach the Fed’s 2% target, a debt crisis arising from unsustainable fiscal spending, the consumer pulling back as savings deplete, oil prices soaring on another geopolitical event, and the Fed not cutting rates as quickly as expected.

As usual, there are a myriad of risks that could reclaim the narrative at any time. Most of these concerns are well understood and not particularly new. Key among them include the lag effect of rate hikes simply postponing the recession, inflation being too sticky to reach the Fed’s 2% target, a debt crisis arising from unsustainable fiscal spending, the consumer pulling back as savings deplete, oil prices soaring on another geopolitical event, and the Fed not cutting rates as quickly as expected.

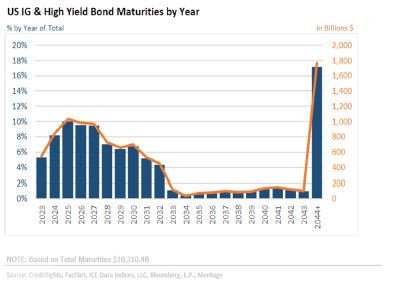

Corporate borrowing costs expected to rise

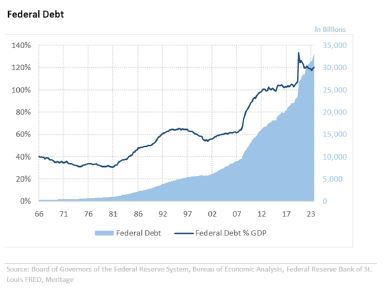

Federal debt as a % of GDP at historic highs

The markets have now priced in six rate cuts for 2024, while the Fed’s revised projections point to three. The strength of the year-end rally and volatility indices registering at multi-year lows would suggest that there is a lot riding on the soft-landing assumption and few if any of the above concerns becoming elevated in the coming year, let alone new risks not yet on anyone’s list.

With respect to portfolio strategy and structure, our quantitative work shows no glaring anomalies in valuation spreads between value and growth stocks. Since growth stocks are still displaying higher free cash flow measures versus historical averages, they remain attractive even after last year’s strong showing. Defensive sectors like Health Care and Consumer Staples are trading at a modest discount, so investors are getting paid to add exposure to these groups as a hedge against a slowing economy. There is support to reduce some exposure from big-cap tech, while at the same time, validating the A.I. story when comparing fundamentals to the extremes of past tech bubbles. In many cases, the beneficiaries of A.I. are businesses that have already been very profitable. This should eventually move down the food chain to smaller companies in the way of enhanced productivity.

Pharma and managed care companies have good valuation support, as do smaller-cap biotech companies. Capital equipment stocks have had a strong tailwind from government funded construction spending, but this will become harder to replicate. Homebuilder stocks, despite their strong performance, continue to be positioned well as the supply of new homes remains constrained and mortgage rates have come off their highs. Lastly, we expect energy to contribute better this year as supply imbalances become more aligned with demand, while geopolitical pressures are not expected to ease.

A quick word on bonds. The prospect of higher bond returns has materialized sooner than expected. The recent collapse of the 10-Year bond yield from 5.0% to 3.8% (almost where it began the year) signals the market’s expectations that the Fed’s battle against inflation is largely complete, and rate cuts will begin in 3-6 months. For additional fixed income commentary, you can either click this link to access Senior Fixed Income Portfolio Manager Chris Hayes’ year-end fixed income overview, or go to the Meritage website Insights page. It was clearly an extraordinary year for the bond market.

We look forward to posting more frequent commentaries covering market activity, portfolio strategy, and wealth management topics as the year progresses. Our best wishes to a great year ahead.